On the 23rd January 2017 the EU Commission issued the “Commission Initiative Roadmap” for 2018 regarding the step up fight against the financing of terrorism, also known as its ‘Payments Restriction Initiative’ or as we are reading more often, the cashless society. This document is an extension of the communication document dated February 2016 (COM-2016/50) and updated to include new regulations for member countries to implement and future intentions by the Commission.

The policy looks to the “Regulation on the controls of cash entering or leaving the Community and relevance of potential upper limits to cash payments.” The Action Plan states that “Payments in cash are widely used in the financing of terrorist activities.” In its conclusions on the fight against terrorism, the Economic and Financial Affairs Council of 12 February 2016 called on the Commission

“to explore the need for appropriate restrictions on cash payments exceeding certain thresholds. In particular the Proposal for an amendment of the Anti-Money Laundering Directive2 (COM (2016) 450), which introduced stricter transparency rules and other measures targeted specifically at terrorism financing. Furthermore, the initiative should be seen in conjunction with the ECB’s decision of 4 May (20163) to discontinue the production of the EUR 500 banknote and stop the issuance of this denomination by around 2018 to address concerns that these notes could be used in financing illicit activities.”

The report goes on to advise that “any measure restricting cash payments would be complementary to the specific actions addressed by the review” and to include “virtual currencies (such as BitCoin) and prepaid instruments (such as pre-paid credit cards) when they are used anonymously.”

New anti-money laundering rules will cover high value goods such as works of art, precious stones or auctioneers, which requires that they apply customer due diligence measures, full identification of customers and keeping records of transactions when receiving cash payments of €15,000 or more.

This latest document extends the cash payments rule by reducing the €15,000 limit on transactions to €10,000 by June 2017.

Unbelievably, the EU Commission is using the logic of banning cash by stating their “remains the lack of readily available and solid evidence on legitimate vs illegitimate cash transactions.” They maintain that “It is difficult to quantify the legitimate or illegitimate use of cash.”

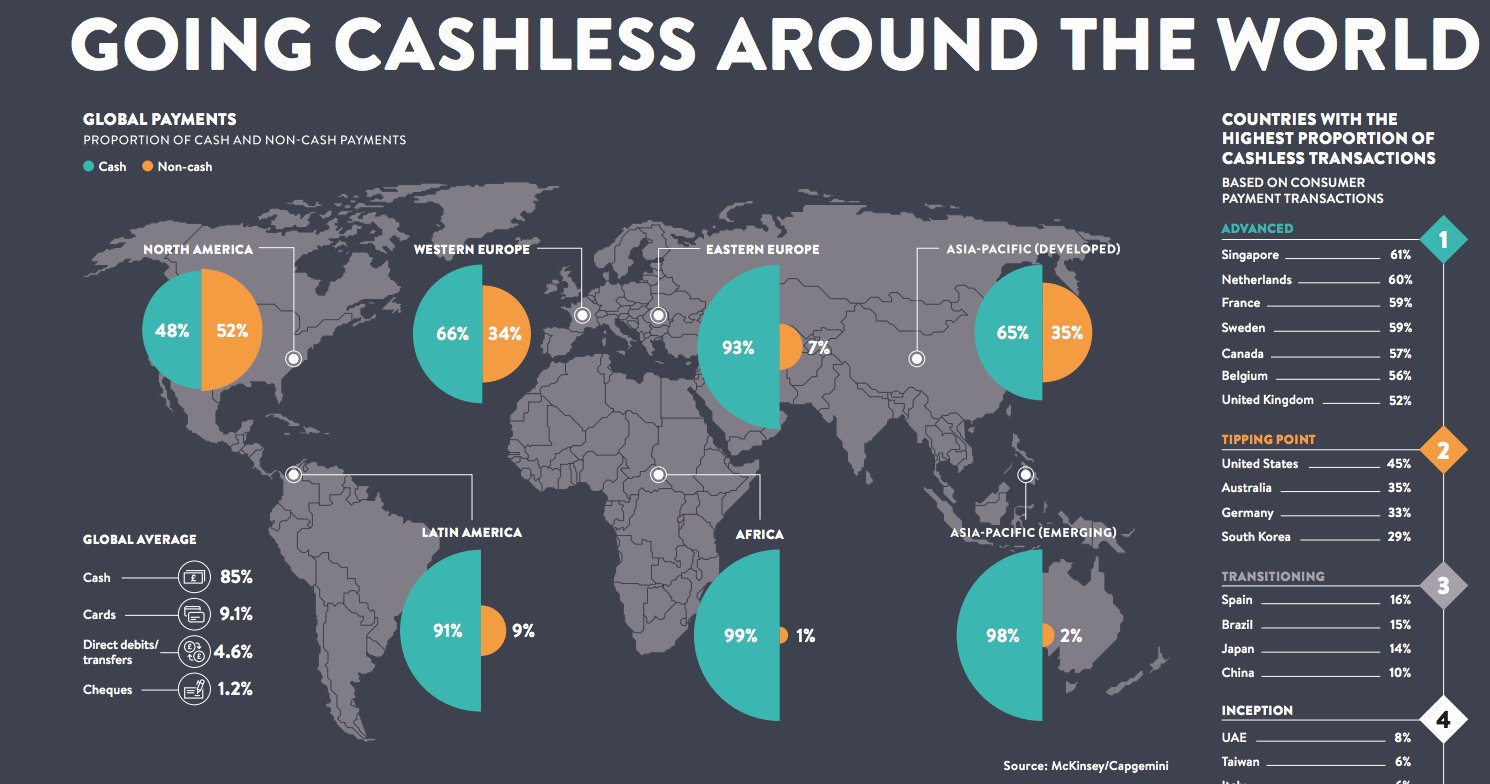

These statements are clearly untrue. Evidence on the amount of cash and how it is used in any given economy is widely known and many government’s even publish it quarterly or annually. For instance, on average, wallets in Germany hold nearly twice as much cash—about $123 worth—as those in Australia, the US, France and Holland, according to a recent Federal Reserve report on how consumers paid for things in seven countries. Roughly 80% of all transactions in Germany are conducted in cash. (In the US, it’s less than 50%.) And cash is the dominant form of payment there even for large transactions.

In Britain, cash payments have fallen to 48% of all transactions – but that is still 18 billion individual transactions made up of £250billion annually. Within those numbers, 10% of all payments were direct debits, like paying for rent, mortgages, utilities and loans. In all countries, estimates of corrupt cash payments are published. Several EU countries, Britain included, even adds illicit transactions such as drugs and prostitution to GDP in an effort to boost published economic performance data.

The EU Commission continues its misinformation campaign by stating that

“Cash has the important feature of offering anonymity to transactions. But, such anonymity can also be misused for money laundering and terrorist financing purposes. The possibility to conduct large cash payments facilitates money laundering and terrorist financing activities because of the difficulty to control cash payment transactions.”

It also does nothing to stop terror-financing and money-laundering, as by far the biggest launderers globally is the Western banking system itself, the EU banks included.

For instance – HSBC admitted to openly laundering billions of dollars for Colombian and Mexican drug cartels and in so doing violated a host of banking laws such as the Bank Secrecy Act to the Trading With the Enemy Act. The USA spent $35 billion in 2015 alone fighting a drugs war only to witness over 9o% of the proceeds of the crimes it was attempting to stop laundered through banks. The fine HSBC received of $1.9 billion, which as one analyst noted is about five weeks of income for the bank is no deterrent. There was so much cash to be laundered that drug dealers specifically designed boxes to fit through the bank’s teller windows and the bank knew where the money was coming from and what accounts to apply it to. The money is then distributed over tax havens and filtered into legal operations the world over. One should note that it is estimated 120,000 have been killed in this drugs war and nearly 30,000 more are missing.

The shift to a cashless society continues to snowball

If the EU Commission wants to stop finance terrorism and money laundering – they need not look further than the Western banking system and its network of tax havens that launders trillions of dollars every single year, as evidenced by this article; Enemies of the State: How The Financial Services Industry Is Destroying Democracy.

Some EU countries are using terrorism as cover for the implementation of its cashless society initiative and already imposed maximum bank withdrawals. Some larger transactions in cash or moving cash from one EU country to another already require the state to be informed. Cash payments for goods and services in France and Italy have been limited to a maximum of €1,000. In Spain the maximum cash transaction is €2500 and no transactions in cash over €15,000 are allowed. The EU is now considering the banning of lower denomination notes than the €500.

“The ECB has already decided to progressively phase out the €500 banknote. But as long as cash exists, large payments will remain possible even with lower denomination banknotes. Therefore there is an option to extend the restrictions to cash payments to all (including crypto) payments.”

The EU Commission is also looking at its legal position that might be, or at least should be challenged. However, the work-around is explained thus:

“While being allowed to pay in cash does not constitute a fundamental right, the objective of the initiative, which is to prevent the anonymity that cash payments allow, might be viewed as an infringement of the right to privacy enshrined in Article 7 of the EU Charter of Fundamental Rights. However, as complemented by article 52 of the Charter, limitations may be made subject to the principle of proportionality if they are necessary and genuinely meet objectives of general interest recognised by the Union or the need to protect the rights and freedoms of others. The objectives of potential restrictions to cash payments could fit such description. It should also be observed that national restrictions to cash payments were never successfully challenged based on an infringement to fundamental rights.”

One point that the EU Commission do not focus on is cybercrime. Europol set up the European Cybercrime Centre (EC3) in 2013 to strengthen the law enforcement response to cybercrime in the EU and thus to help protect European citizens, businesses and governments from online crime. Cybercrime costs EU Member States EUR 265 billion a year. And that’s just the financial side. There is no contingent for a financial cyber-attack from say Russia, the latest arch enemy that seems able, according to the CIA and FBI, to decide who gets into office in Washington DC. If a foreign enemy state was indeed able to successfully launch such an attack it would bring any country to its knees within days if there was no cash moving around the economy as society would be entirely dependent on an electronic payments system.

The document ends with the observation that depending on the complexity of the final proposal and the legal instrument used, an implementation plan is not just feasible it might well be established quite quickly. The EU’s war on cash and desire to control citizens through a cashless-society model is snowballing without a real open debate with its people.

The original source of this article is True Publica

Copyright © Graham Vanbergen, True Publica, 2017

Credit to globalresearch.ca

http://www.globalresearch.ca/eu-steps-up-the-pace-for-cashless-society-in-201718/5573210

No comments:

Post a Comment