Tuesday, November 25, 2014

"Britain Is In The Wrong Place,"... "The World Economy Has Left Europe Behind"

I love the idea that prosperity can be decreed by a G20 communiqué. World leaders in Brisbane have airily committed themselves to two per cent growth. (Why only two per cent? Why not 20 per cent? Or 200 per cent? Who knew it was so easy?) Meanwhile, in the real world, the divergence between Continental Europe and the rest of the planet accelerates.

The Eurozone has technically avoided its third recession in six years. Having contracted sharply in the second quarter of this year, it managed 0.2 per cent growth in the third. But it seems unable to shake off its debilitating condition.

Six years after the credit crunch, every other continent has recovered robustly. Europe alone appears to have contracted a chronic disease.

That infection has spread right across the continent. By far its three largest economies are France, Italy and Germany, accounting among them for two thirds of the Eurozone. All three are experiencing recurring bouts of illness.

France managed to return to growth largely because of a massive injection of government cash in healthcare. This, though, is hardly a solution. Au contraire, it is more of the medicine that sickened the patient. France last ran a balanced budget in 1974. This can’t carry on.

Italy has now contracted for 12 consecutive quarters. Indeed, to a single approximation, it has not grown since the euro was launched.

But if the malaise in France and Italy was predictable, Germany’s slowdown is a shock. Until now, the EU’s largest state had been carrying the single currency. It acted partly from a sense of historical responsibility – a sincere if incorrect belief that European integration made war less likely – and partly because, so far, the euro has brought advantages to Germany.

It’s true that the meltdown in the Mediterranean forced German taxpayers to write out IOUs to more profligate governments. But it also pushed down the value of the single currency, thus allowing German exporters to benefit from an artificially cheap exchange rate.

So far, like Atlas, Germany has been able to bear the weight of the euro on its shoulders. But it’s starting to sweat and sway. German exports, hitherto the Eurozone’s great success story, are now falling faster than at any time since the global crisis began.

Some blame the tit-for-tat economic sanctions with Russia, imposed because of the war in Ukraine. Others argue that a weak euro disguised the effect of years of underinvestment. Whatever the explanation, German analysts have slashed their growth forecasts. A report by the country’s five leading economic institutes, the so-called Wise Men, says that the economy has “stagnated”, and predicts a rise in unemployment.

We can’t console ourselves with the thought that the Eurozone has been failing to recover because it has been concentrating on paying off its debts. On the contrary, borrowing continues to grow. Bad debt at Eurozone banks is now estimated to be 18.9 per cent higher than previously thought, at about 880 billion euros – equivalent to nine per cent of the entire Eurozone economy. Italy’s national has grown to 133 per cent of GDP; Belgium’s to 107 per cent.

It’s no longer credible to keep blaming the sub-prime crisis. Every other continent has bounced back convincingly. So, indeed, has Britain, which is now the fastest-growing economy in the G7. The EU’s problems are older and deeper than the credit crunch.

The long-term indicators for Europe are dire. While the single currency has certainly accelerated the EU’s economic decline, it did not cause it. The underlying problem may be simply stated. Too few people are generating wealth and too many are consuming it. Europeans are spending more and more time in education, and living longer and longer after they retire. Many of them spend the few years in between working for the government.

Europe’s working age population peaked in 2012 at 308 million, and will fall to 265 million by 2060. The ratio of pensioners to workers will, according to The Economist, rise from 28 per cent to 58 per cent – and even these statistics assume the arrival of a million immigrants every year.

Emmanuel Todd, arguably France’s leading demographer, has observed that these figures disguise big variations within Europe: Britain and Scandinavia have much younger populations than the Continent. He points out that the Anglosphere – the United States, Canada, Australia, New Zealand and Britain – will soon be more populous than mainland Europe, and concedes that Britain would be better off with the other English-speaking democracies.

He’s right. We are now members of the only trade bloc on the planet that is shrinking. The calculation we made when we joined what was then the EEC in 1973 turned out to be wrong.

Back then, we looked across the Channel and saw what looked like a thundering success story. We noticed that our pounds were worth less and less each time we visited Germany, and read clever articles about how the “Rhineland model” of economics was better than our own. We decided to hitch our carriage to what seemed the most powerful locomotive on the planet.

In retrospect, our timing could hardly have been worse. Western Europe had indeed spectacularly outperformed the UK between 1945 and 1973, as it bounced back from the artificial low of the Second World War. Britain, in contrast to most Continental states, had amassed a colossal debt in the struggle against Hitler, and spent the next three decades inflating it away, with calamitous effects on our economy.

But the picture changed with the oil shock of 1974. Suddenly, Western Europe was no longer the runaway success we thought. Far from hitching our carriage to a locomotive, we had shackled ourselves to a corpse.

Worse, we had done so at precisely the moment when common-law and English-speaking economies around the world were beginning a growth spurt that endures to this day. In 2013, the Commonwealth’s economy overtook the Eurozone’s.

All the core Anglosphere countries are projected to grow next year by between 2.5 and 3.1 per cent. India, according to the IMF, will grow at 6.4 per cent. But we can’t sign a bilateral free trade agreement with any of these countries. We surrendered our trade policy to Brussels on 1 January 1973.

The case for being in the EU has been overtaken by technology. You could just about make the argument, in the early 1970s, that regional trade blocs were the way forward. But no one seriously believes that in the Internet age. Geographical proximity has never mattered less.

Perhaps, decades from now, the past 40 years, during which we sundered ourselves from our hinterland and artificially redirected our trade to Europe, will be seen as an aberration. When Charles de Gaulle vetoed our entry into the EEC, he gave a very good reason. Britain, he explained was “insular, maritime and linked by her exchanges, her markets and her supply routes to the most diverse and often farthest-flung of nations.”

Indeed. And those far-flung nations would make a far more natural trade bloc than the EU, bound as they are by language and law, habit and history. After all, the whole purpose of commerce is to swap on the back of differences. It never made much sense to abandon a diverse market, which comprised agricultural, industrial and service economies, in favour of a union of similar Western European states.

David Cameron can hardly have failed to notice, as he looked around the G20 table, that his European colleagues are the ones with the worst problems. Britain is in the wrong place.

Credit to Zero Hedge

HOW TO AVOID BEING SENT TO A FEMA CAMP

“God grant me the serenity to accept the things I cannot change; the courage to change the things I can; and the wisdom to know the difference.“

Serenity Prayer

There are certain realities that are transpiring in the world today that none of us has any control over. The only thing that we have control over is our reaction to the events that we have no control over. We live in a world where the majority of our fellow citizens have chosen the life of sheep. It is a life that is devoid of insight, discernment, moral and physical courage.

When the riots begin in Jefferson, you need not fan the flames. Stay home and protect your family by all means necessary. And there is a another lesson to learn be not living in the matrix of evil, you will discover how to avoid being sent to a FEMA camp.

The Common Sense Show: Freeing America One Enslaved Mind At a Time

In my life as life as advocate for fairness and justice, I used to believe and have as a life’s mission that if I could wake up enough people as to the matrix of evil that we are all living in, that humanity would throw off our collective chains of enslavement and we could conquer evil and establish a more sane system than the world we find ourselves hopelessly trapped inside of.

For years, I have tried to lead a revolution of consciousness which sought to gain momentum and stop evil in its tracks. I now realize I was embracing a fool’s errand. When we, as a nation, accepted the murder of 53 million innocent Americans since 1972, we spat upon the word of God. When we, as a nation, allowed our leaders to conduct wars of occupation for fun and profit which resulted in the deaths of millions of innocent people,we became accomplices to genocide. When you allow your children to attend a school which teaches third graders about oral sex and condoms, we are preparing our children to inherit a world based upon depravity and abject satanically inspired evil.

Focus on Changing the Things You Can Change

The longer that I am engaged in the fight against evil, the more I begin to see the wisdom of the Bible. Galatians 5:1 states that “For freedom Christ has set us free; stand firm therefore, and do not submit again to a yoke of slavery.” I have the peace of mind to know that I do not live in the matrix of evil and I am not blinded by the trappings of this life. I will never submit despite the fact evil dominates the halls of Congress, the White House. I am reminded by the media on a daily basis about just how fun evil is.

I have forsaken the belief that I can change the world. All I can do is to save my soul and share my observations and experiences with a few other people in the hope that we can help each other reach a higher level of spiritual existence. For example, we all know that violence begets nothing but violence. No matter how justified or how unjust the killing of a 18 year old boy may be in Ferguson, MO., your violence will not change what has happened. Your participation under the encouragement of the agents of antagonism which have been sent to Ferguson in order whip up the people into a riotous mentality of senseless violence, serves nobody but the evil intentions of those presently in power. These agents of evil seek to promote a civil war and they seek to divide and conquer us along racial lines, so that they can enact their martial law plans which involves the activation of the FEMA camps that I have written and documented so many times. Make no mistake about it, Ferguson is not its own end. It is the means to an end which ends in our total enslavement.

To all black, white, brown and yellow people, evil seeks to divide us and use as their instrument of terror civil unrest based upon racism and unwarranted fear. All we have to do is sit at home and say no this insanity in order for this to go away. As the Jefferson verdict is announced, sit by your door with your shotgun, in order to keep evil out, but do not feed evil by entering the streets. And while you are sitting at home today, pray for peace and for the discernment of the people in order that they will not be used by the thugs that have been sent to agitate. There is power in collective prayer. Today is the day we can take a stand against evil by refusing to participate.

How to Avoid Being Sent To a FEMA Camp

Aleksandr Solzhenitsyn once said that “Violence can only be concealed by a lie, and the lie can only be maintained by violence” Do you want to stay out of a FEMA detention camp? Then stay off the streets in Ferguson or wherever ACORN, the New Black Panthers and the Agents Provocateur from DHS are attempting to wreak their havoc. If we stay off of the streets in places like Ferguson, then there are no riots, there is no martial law, there are no roundups and the camps will sit empty and nobody has to die,at least not today.

We do live in a time that the FEMA camps are indeed being activated. This is a time that Solzhenitsyn lived through as he and so many others were taken to the Soviet Gulag. After being incarcerated, Solzhenitsyn lamented that they should have fought back in their homes as the KGB came to claim their freedom. He once said “that if we could have make them wonder if they were going home to their families, we might have stopped the insanity”. When they do come for you, resisting in your doorway provides you with a better fate than what lies on the other side of the barbed wire.

Conclusion

Acceptance is about taking charge of the direction of our lives and making conscious decisions to not be taken off of the path that God has planned for us. We are not cursed, we are not victims of life, and no one is punishing us. We simply cannot stop evil, only the Second Coming of Christ can accomplish that goal. Acceptance is the recognition that our souls have been placed here by the Almighty to learn specific lessons. How to deal with evil is one of these lessons. We can only control our reaction to evil by refusing to participate in the evil and then resist with everything you have when evil comes looking for you in your home. For if you do these things, you need never worry about being sent to a FEMA camp. More importantly, if you do these things, you will not lose your soul.

Credit to Common Sense

Right-Wing Leader Marine Le Pen Demands Central Bank Repatriate French Gold

First Germany, then the Netherlands, perhaps Switzerland this weekend, and now the French right-wing Front National, which shockingly came first in May's European parliament elections, and whose leader Marine Le Pen is currently polling in first place in a hypothetical presidential election (in both a first and run off round), ahead of president Hollande, has sent a letter to the governor of the French Central Bank, the Banque de France, demanding that France join the list of nations which have repatriated, or at least tried to, their gold.

From her letter, here is the full list of French demands (google translated):

- Urgent repatriation on French soil of all of our gold reserves located abroad.

- An immediate discontinuation of any gold sales program.

- Conversely, a gradual reallocation of a significant portion of foreign exchange reserves in the balance sheet of the Bank of France by buying gold at each significant decrease in the price of an ounce (recommendation 20%) .

- A suspension of any financial commitment or loan contract would wager that our gold reserves.

- At the patrimonial and financial balance of the 2004 gold sales transactions ordered by N. Sarkozy.

Her full letter below (link)

Mr. Christian Noyer

Governor of the Banque de France

31 rue Croix des Petits-Champs

75049 PARIS Cedex 01

31 rue Croix des Petits-Champs

75049 PARIS Cedex 01

Nanterre, November 24, 2014

Open letter to Mr Christian Noyer on the gold reserves of France

Dear Governor

On behalf of the French and in my capacity as the main opposition leader, I am writing to you because it is my duty to present a petition on the gold reserves of France, under the best interests of our nation.

Even before the outbreak of the 2008 crisis, the National Front had anticipated and informed the political institutions of the future worsening of the macro-economic and geopolitical context. As part of the business model increasingly libertarian adopted by France under pressure from Brussels, no economic fundamentals may not sustained improvement. All French can see that the austerity policies demanded by the EU and the ECB and implemented by the government are a proven failure and serious for our country.

The monetary institution you lead a historic mission to be the custodian of national central bank monetary reserves including gold reserves. According to our strategic vision and sovereign, they are neither the state nor the Bank of France but the French people and in addition serve as the ultimate guarantee of public debt and our currency.

In monetary Cold War played between the Western countries and the BRICS countries, gold gradually takes an important role. According to the World Gold Council, China's official gold reserves, India and Russia have increased significantly between 2007 and 2013.

For these reasons and because of the rapid growth of global systemic risk, it is of utmost importance to the future solvency of our nation to engage, by mid-2015, a detailed audit procedure, the results will be the subject of a report. This report must obtain validation of French macro-prudential authorities, ACPR, and will be made public in the year.

For these reasons and because of the rapid growth of global systemic risk, it is of utmost importance to the future solvency of our nation to engage, by mid-2015, a detailed audit procedure, the results will be the subject of a report. This report must obtain validation of French macro-prudential authorities, ACPR, and will be made public in the year.

This comprehensive audit should contain:

- A complete inventory of physical gold amounts to 2435 tons currently displayed and their quality (serial number, purity, bars 'Good Delivery' ...), conducted by an independent French body (to be defined). This inventory, under supervision of a bailiff, must indicate the country in which the gold reserves are stored in France or abroad.

- A census of all formal financial employment agreement or secret vis-à-vis private banks and corporations, or bilateral loan between France and national and international institutions, having pawned the gold of France to ensure rescue of the euro. In this case, the comprehensive audit should contain the conditions of agreement or loans.

Furthermore:

Whereas, on 30 November, will take place in Switzerland a vote on a request from popular initiative referendum "Save gold for Switzerland" of the UDC party (Democratic Union of the Centre) which provides for the repatriation of their reserves of gold on their soil.

Whereas at the request of some national central banks informed, this country phenomenon for the "return of national gold reserves" and democratic control exists since 2013 in Germany (Bundesbank), Poland etc.

Whereas the Dutch Central Bank recently said it had repatriated 122.5 tons of gold.

Whereas, on 19 May 2014 the Bank of France along with other banks of the Eurosystem, announced it has signed the Washington Agreement gold sales CBGA 4 (Dirty Gold Under the Central Bank Gold Agreements) which provides no transfer of quotas on this five-year period (2014-2019), in contrast to the three previous agreements.

Whereas in fact, the Bank of France already independent, conducted as part of the agreement CBGA 2 on gold sales agreed in 2004 by Nicolas Sarkozy, then Minister of Economy and Finance of the Raffarin government .

The declared official target of more actively manage the foreign exchange reserves of the state to generate € 100 million in additional tax revenue in 2005. N. Sarkozy also said that gold sales would be used "either to finance investments that prepare the future, either to reduce the debt, but in no case to fund operating expenses. "

Over the period 2004-2012, about 614.6 tonnes of gold were sold by France, while at the same time the other central banks of the Eurosystem with the ECB have agreed to limit their gold sales. According to a report of the Court of Auditors in 2012, this operation is extremely costly for public authorities and constitutes a serious violation of the national heritage, made without any democratic consultation.

Mr Governor, according to your statements, "gold remains an important element of global monetary reserves." For the French, you are considered the ultimate guarantor of the security of this gold reserve and therefore the stability of our currency and national financial stability. As a result, your responsibility is huge.

Also, depending on the situation we discover, I urge you to do it:

- Urgent repatriation on French soil of all of our gold reserves located abroad.

- In immediate discontinuation of any gold sales program.

- Conversely, a gradual reallocation of a significant portion of foreign exchange reserves in the balance sheet of the Bank of France by buying gold at each significant decrease in the price of an ounce (recommendation 20%) .

- A suspension of any financial commitment or loan contract would wager that our gold reserves.

- At the patrimonial and financial balance of the 2004 gold sales transactions ordered by N. Sarkozy.

The implementation of these measures is crucial for the future of France face socio-economic problems that may occur.

Just like your heroic predecessors of the Bank of France in 1939 and 1940 had organized the evacuation of French gold, you need to undertake this vast national treasure of the security operation, patriotic act which will be recognized in due time by the public opinion.

I sincerely hope that, respectful of your duties as a senior official in the service of the state, you demonstrate lucidity and courage necessary for the defense of the general interest of our country. The stakes are high, it is the future of France in question!

Please accept, Excellency the Governor, the assurances of my highest consideration.

Marine Le Pen

Credit to Zero Hedge

The actions of central bankers around the globe are signs of desperation

The actions of central bankers around the globe which have been driving stock prices higher are not a sign of control. They are signs of desperation. They are losing control. Their academic theories have failed. Their bosses insist they turn it up to eleven. Something is going to blow. You can feel it. John Hussman knows what will happen. Do you?

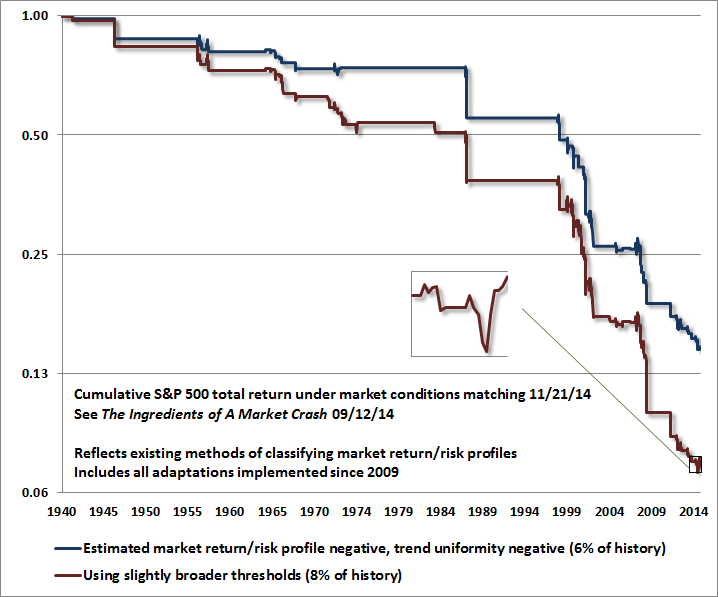

That said, it’s worth noting that the inclinations of central banks toward quantitative easing and interest rate suppression are increasingly taking on a tone of desperation in the face of accelerating economic weakness in Japan, Europe and China.While the stated objective is to increase inflation, low inflation isn’t really the economic problem – low growth, intolerable debt burdens, and misallocated capital are at the core of global challenges here. Unfortunately, QE only misallocates capital toward more speculation and low-quality debt (primarily junk and leveraged loan issuance), without much impact on real growth. China’s move was prompted in part by a surge in bad loans to the highest level in nearly a decade. The largest European banks now have gross-leverage ratios as high as 30-to-1 (during the credit crisis, one could order the sequence of defaults accurately using this metric, with Bear Stearns, Lehman, and Fannie Mae right at the top). But liquidity does not create solvency, and with credit spreads widening, the growing desperation of monetary authorities is more a negative signal than a positive one.This is much like what we saw in 2007-2008: when concerns about default are rising, default-free, low-interest rate money is not considered to be an inferior asset, and as a result, its increased availability does not provoke risk-seeking behavior. If we observe narrowing credit spreads and stronger uniformity in market internals, we will be able to infer a shift toward risk-seeking (and in turn, a greater likelihood that monetary easing will provoke further speculation). That won’t make stocks any cheaper, and downside risk will still need to be managed, but our immediate concerns would be less dire. At present, current market conditions and the lessons of history encourage us to be aware that very untidy market outcomes could unfold in very short order.The upshot is this. Quantitative easing only “works” to the extent that default-free, low interest liquidity is viewed as an inferior holding. When investor psychology shifts toward increasing risk aversion – which we can reasonably measure through the uniformity or dispersion of market internals, the variation of credit spreads between risky and safe debt, and investor sponsorship as reflected in price-volume behavior – default-free, low-interest liquidity is no longer considered inferior. It’s actually desirable, so creating more of the stuff is not supportive to stock prices. We observed exactly that during the 2000-2002 and 2007-2009 plunges, which took the S&P 500 down by half in each episode, even as the Fed was easing persistently and aggressively. A shift toward increasing internal dispersion and widening credit spreads leaves risky, overvalued, overbought, overbullish markets extremely vulnerable to air-pockets, free-falls, and crashes.

Deutsche Bank's Modest Proposal To Central Banks: "Purchase The Gold Held By Private Households"

From the bank that a few days ago informed us that "People Are Talking About Helicopter Money And Debt Cancellation Being The End Game", comes the logical next step. Here it is, without commentary and the key section highlighted:

From Deutsche bank Behavioral Finance: Daily Metals Outlook

Although gold market operators are currently pre-occupied with the prospect of the SNB finding itself obliged by referendum to buy large quantities of bullion, another central bank raised the same possibility yesterday: the ECB. As odd as it sounds, given the contentious internal debate this year over asset purchases in general, ECB board member, Yves Mersch, reminded journalists that the Bank could in theory buy any asset within a QE program. This could mean government debt, equities, ETFs, or even gold. Indeed, within an effective asset purchase program it matters not so much what the asset is, than who the seller is. Given that the eurozone banking system still appears to be a bottleneck in the monetary transmission mechanism, there might be some wisdom in bypassing it. Banks do not hold gold. However, this ‘theoretical’ possibility would quickly run into practical constraints, not least the volume limitations and the problem of having to pick winners and losers.However, the idea of gold purchases has merit because of the possible sellers. Much gold is held in private households, especially in countries like Germany. In some cases these are unwanted remnants of crisis-driven investments five years ago. A program that targeted these holdings would liberate dormant liquidity, some of which might even flow into consumption.

In other words, all the world's central banks would need to do to "liberate dormant liquidity" , held, as DB suggests, by private households in various "unwanted" troves of physical gold, and in the process also build up their gold holdings, would be to make said gold unattractive to hold.

And if that fails, well, FDR already showed the world how to deal with an intransingent public which does not want to part with its gold in Executive Order 6102, something which the Dutch Central Bank which also made the news recently when it secretly repatriated 122 tons of gold from the NY Fed, already did years ago when it advised pension funds to sell their gold: confiscation Credit to Zero Hedge

Subscribe to:

Posts (Atom)