The actions of central bankers around the globe which have been driving stock prices higher are not a sign of control. They are signs of desperation. They are losing control. Their academic theories have failed. Their bosses insist they turn it up to eleven. Something is going to blow. You can feel it. John Hussman knows what will happen. Do you?

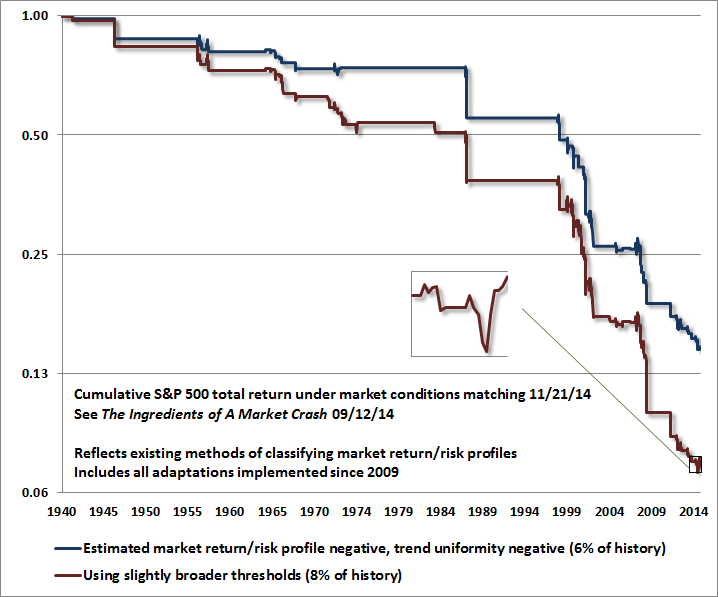

That said, it’s worth noting that the inclinations of central banks toward quantitative easing and interest rate suppression are increasingly taking on a tone of desperation in the face of accelerating economic weakness in Japan, Europe and China.While the stated objective is to increase inflation, low inflation isn’t really the economic problem – low growth, intolerable debt burdens, and misallocated capital are at the core of global challenges here. Unfortunately, QE only misallocates capital toward more speculation and low-quality debt (primarily junk and leveraged loan issuance), without much impact on real growth. China’s move was prompted in part by a surge in bad loans to the highest level in nearly a decade. The largest European banks now have gross-leverage ratios as high as 30-to-1 (during the credit crisis, one could order the sequence of defaults accurately using this metric, with Bear Stearns, Lehman, and Fannie Mae right at the top). But liquidity does not create solvency, and with credit spreads widening, the growing desperation of monetary authorities is more a negative signal than a positive one.This is much like what we saw in 2007-2008: when concerns about default are rising, default-free, low-interest rate money is not considered to be an inferior asset, and as a result, its increased availability does not provoke risk-seeking behavior. If we observe narrowing credit spreads and stronger uniformity in market internals, we will be able to infer a shift toward risk-seeking (and in turn, a greater likelihood that monetary easing will provoke further speculation). That won’t make stocks any cheaper, and downside risk will still need to be managed, but our immediate concerns would be less dire. At present, current market conditions and the lessons of history encourage us to be aware that very untidy market outcomes could unfold in very short order.The upshot is this. Quantitative easing only “works” to the extent that default-free, low interest liquidity is viewed as an inferior holding. When investor psychology shifts toward increasing risk aversion – which we can reasonably measure through the uniformity or dispersion of market internals, the variation of credit spreads between risky and safe debt, and investor sponsorship as reflected in price-volume behavior – default-free, low-interest liquidity is no longer considered inferior. It’s actually desirable, so creating more of the stuff is not supportive to stock prices. We observed exactly that during the 2000-2002 and 2007-2009 plunges, which took the S&P 500 down by half in each episode, even as the Fed was easing persistently and aggressively. A shift toward increasing internal dispersion and widening credit spreads leaves risky, overvalued, overbought, overbullish markets extremely vulnerable to air-pockets, free-falls, and crashes.

Deutsche Bank's Modest Proposal To Central Banks: "Purchase The Gold Held By Private Households"

From the bank that a few days ago informed us that "People Are Talking About Helicopter Money And Debt Cancellation Being The End Game", comes the logical next step. Here it is, without commentary and the key section highlighted:

From Deutsche bank Behavioral Finance: Daily Metals Outlook

Although gold market operators are currently pre-occupied with the prospect of the SNB finding itself obliged by referendum to buy large quantities of bullion, another central bank raised the same possibility yesterday: the ECB. As odd as it sounds, given the contentious internal debate this year over asset purchases in general, ECB board member, Yves Mersch, reminded journalists that the Bank could in theory buy any asset within a QE program. This could mean government debt, equities, ETFs, or even gold. Indeed, within an effective asset purchase program it matters not so much what the asset is, than who the seller is. Given that the eurozone banking system still appears to be a bottleneck in the monetary transmission mechanism, there might be some wisdom in bypassing it. Banks do not hold gold. However, this ‘theoretical’ possibility would quickly run into practical constraints, not least the volume limitations and the problem of having to pick winners and losers.However, the idea of gold purchases has merit because of the possible sellers. Much gold is held in private households, especially in countries like Germany. In some cases these are unwanted remnants of crisis-driven investments five years ago. A program that targeted these holdings would liberate dormant liquidity, some of which might even flow into consumption.

In other words, all the world's central banks would need to do to "liberate dormant liquidity" , held, as DB suggests, by private households in various "unwanted" troves of physical gold, and in the process also build up their gold holdings, would be to make said gold unattractive to hold.

And if that fails, well, FDR already showed the world how to deal with an intransingent public which does not want to part with its gold in Executive Order 6102, something which the Dutch Central Bank which also made the news recently when it secretly repatriated 122 tons of gold from the NY Fed, already did years ago when it advised pension funds to sell their gold: confiscation Credit to Zero Hedge

No comments:

Post a Comment